I. BRIEF NOTES ON THE PRINCIPAL TAXES THAT MUST BE PAID:

1) VAT (Value Added Tax): You will be subject to the regular rate of 10%. There are also additional rates of 5% and 0%, as well as a VAT exemption. Payment is due every quarter (the last day of the following month of quarter).

2) CIT (Corporate Income Tax): The taxable income is subject to a standard rate of 20% CIT. The final day of the month after the end of each quarter is when payments are due, and there are 90 days for year-end finalization.

Expenses that satisfy the following criteria are CIT deductible:

– relevant to company operations;

– having enough valid invoices;

– using non-cash payment methods following tax regulations.

3) PIT (Personal income tax):

a) Flat rate 20% for non-resident employees

b) Flat rate 10% for resident employees not having labor contracts

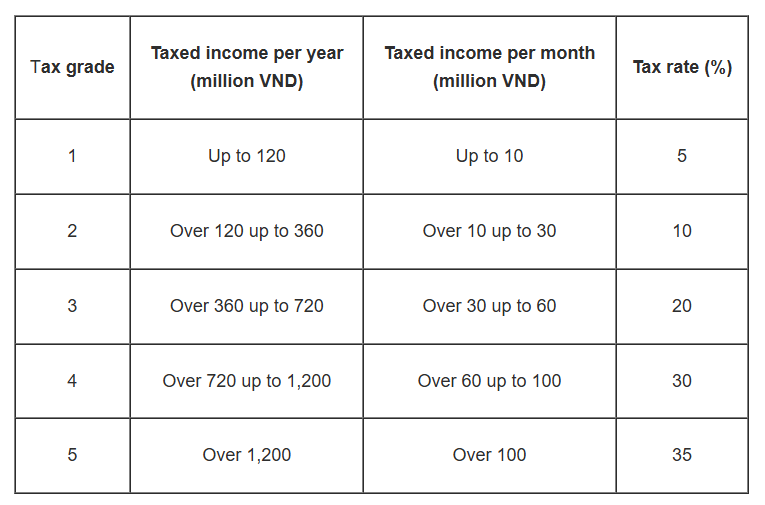

c) For residents with labor contracts, shall apply the progressive tax rates:

II. BRIEF NOTES ON THE SOCIAL-HEALTH-UNEMPLOYMENT INSURANCE (SHUI) THAT MUST BE PAID

1. Expats’ mandatory insurance rates:

2. Local employee’ mandatory insurance rates:

The payment timeline is monthly (the last day of each month).

III. BRIEF NOTES ON THE TRADE UNION FUND THAT MUST BE PAID

Employers contribute to trade union funds at a rate of 2% on salary funds based to pay social insurance for employees. The payment plan is monthly (the last day of each month).